Contents

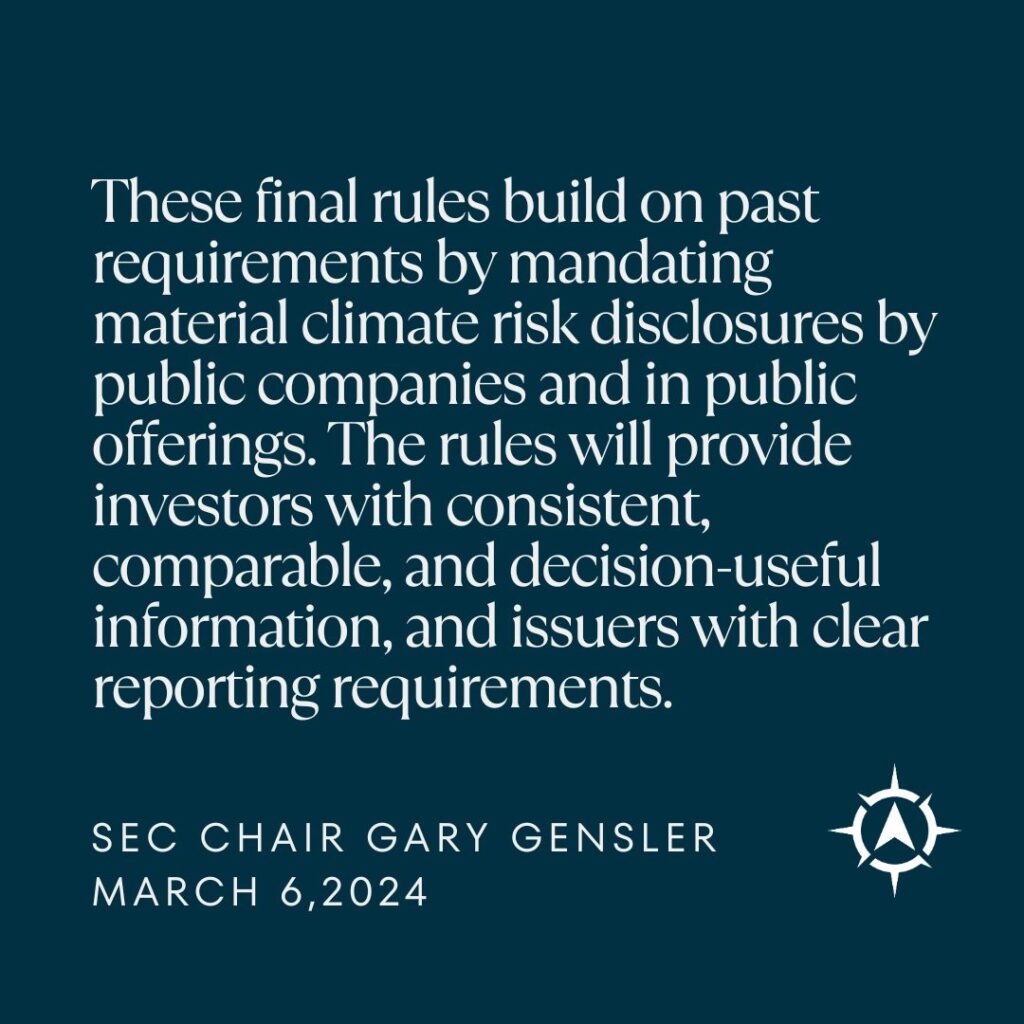

The verdict is out! In a historic decision, the Securities and Exchange Commission (SEC) announced its final regulations on March 6th, 2024. These climate disclosure rules will revolutionize corporate transparency like never before! The SEC’s approach carefully balances the need for comprehensive environmental data with considerations of the cost and complexity of reporting.

These 9 key takeaways shed light on the finalized regulations, revealing the potential implications of the final proposed rule and changes for businesses and investors alike. Here are the key points from the freshly adopted rules:

1. Scope 1 and 2 Disclosure Requirements: The SEC has adopted new rules to standardize and improve climate-related disclosures by public companies. Businesses are required to disclose both their Scope 1 and Scope 2 emissions. Scope 1 emissions originate from sources that are directly controlled or owned by a company. Conversely, Scope 2 emissions are indirect emissions arising from the company’s consumption of purchased electricity, heating, and cooling, stemming from their generation. This requirement ensures investors can access data reflecting the company’s direct and indirect energy consumption and greenhouse gas emissions footprint.

2. Scope 3 Emissions Reporting: Under the SEC’s climate disclosure rule, the explicit requirement for Scope 3 emissions reporting has been dropped following extensive public feedback. However, the emphasis on comprehensive climate-related disclosures remains. Scope 3 includes all other indirect emissions within a company’s value chain. While not mandated, reporting these emissions is strongly encouraged for companies where Scope 3 constitutes a significant portion of their carbon footprint.

3. Investor-Driven Change: The SEC has issued a rule that enhances and standardizes climate-related disclosures. The process attracted the attention of various stakeholders, including companies, auditors, legislators, and trade groups, all of whom contributed to the conversation and outcome. After an extended public comment period that included almost 24,000 comments, the Scope 3 requirement was dropped. In the wake of the decision, it is undeniable that the remarkable volume of feedback reflects a high level of interest and brought forth diverse perspectives on how climate-related risks should be reported and managed within the financial sector.

4. Material Risk Disclosure: Companies must now disclose climate-related risks that are significantly affecting their operations, focusing on current and future impacts. This will ensure stakeholders are informed about potential challenges and opportunities related to climate change. Further, these disclosures detail how these factors could impact the company’s strategy, operational effectiveness, and long-term sustainability. This effort aligns with the broader goal of incorporating relevant risk management procedures into the corporate framework. By making material risk disclosures a staple of their financial reporting, companies affirm their commitment to transparency and accountability, paving the way for more informed investment decisions.

5. Governance of Climate Risks: Companies must also provide insights into the board’s oversight of climate risks with the role of management in climate risk management clearly outlined. A company must outlay a company’s organizational structures, processes, and positions or committees responsible for climate risk management. This reporting will make certain that investors understand the company’s commitment to effective governance and risk management related to climate change.

6. Targets and Goals Transparency: Under the SEC’s climate disclosure decision, companies must disclose their climate-related targets, including their anticipated financial and operational impacts, as part of their audited financial statements. Examples of targets include lowering greenhouse gas emissions, shifting towards renewable energy sources, or attaining carbon neutrality. By integrating these disclosures, companies affirm the seriousness of their commitment to these targets under the rigorous scrutiny of financial reporting standards set forth by the Securities Exchange Act.

7. Financial Impacts of Climate Events: Companies, especially large accelerated filers, must detail financial losses from severe weather and natural hazards in their annual reports, enhancing risk assessment and providing reliable information to investors. As a tool for assessing potential financial impacts under various climate-related scenarios, scenario analysis improves the knowledge of a company’s threshold for climate change. Further, companies are expected to disclose GHG emissions targets in their broader climate strategy. This comprehensive approach ensures that stakeholders are informed of the immediate financial impacts of climate-related events and the company’s long-term commitments to reducing its environmental footprint through specific GHG emissions targets.

8. Inclusion in SEC Filings: The rules aim to elevate the reliability of reported information by integrating climate disclosures, including scenario analysis, into formal filings with the Securities and Exchange Commission. This approach ensures that investors receive comprehensive and dependable insights directly within the framework of SEC regulations.

9. Phased Compliance: The SEC’s climate-related disclosure rules mark a significant step forward in the fight against climate change, setting definitive reporting obligations for companies. To ensure clarity and provide a manageable transition, the SEC has implemented staggered compliance dates for different categories of filers.

Phased Compliance Timeline – 1

This phased approach is designed to provide companies with the necessary time to adapt, ensuring they are well-prepared to meet the new demands. This structured timeline reflects the SEC’s understanding of the operational challenges companies face. By providing a clear and extended compliance window, businesses can allocate resources more effectively, implement comprehensive reporting systems, and ensure the accuracy of their climate-related disclosures. This measured rollout aims to foster a robust framework where companies can meet their obligations without undue strain, ultimately contributing to a more transparent and sustainable business environment.

1. Scope 1 and Scope 2 Reporting: Larger companies will be required to report on climate-related data for both Scope 1 (direct emissions from their operations) and Scope 2 (indirect emissions from purchased energy).

2. Disclosure of Climate-Related Targets or Goals: Companies must provide information on any climate-related targets or goals that are material to their business, results of operations, or financial condition.

3. Governance and Oversight: The rule emphasizes disclosure about the board of directors’ oversight of climate-related risks and management’s role in managing these risks.

4. Phased Implementation: The rule will be phased in, starting in 2026. It will require companies to disclose climate action, greenhouse gas emissions, and financial impacts related to severe weather events.

5. Scenario Analysis: Companies must perform scenario analysis to assess the impact of different climate-related scenarios on their business. This includes evaluating risks and opportunities associated with climate change.

6. Physical Risks: Disclosure should include physical climate change risks like natural disasters and rising sea levels.

7. Transition Risks: Companies need to disclose transition risks, including those related to policy changes, technological advancements, and market shifts due to climate-related factors.

8. Supply Chain Risks: Companies should assess and disclose climate-related risks in their supply chains, including vulnerabilities related to suppliers’ operations and dependencies.

9. Metrics and Targets: Companies must disclose specific metrics related to emissions, energy usage, and other climate-related factors. Setting science-based targets is encouraged.

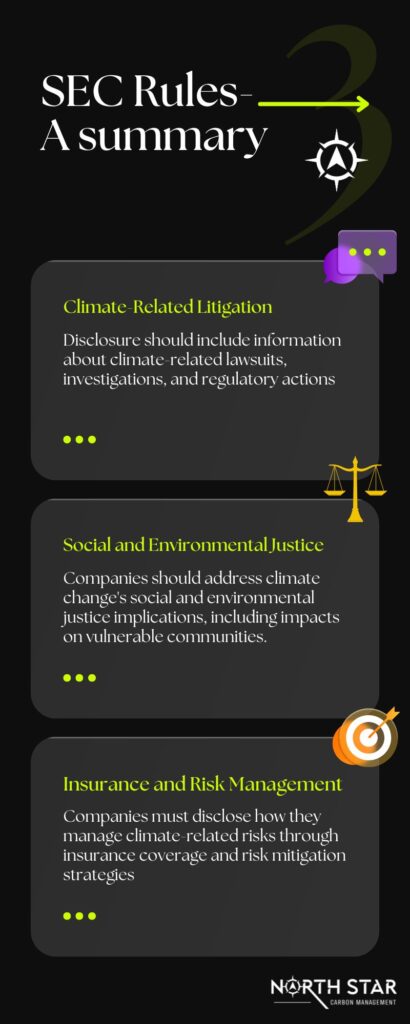

10. Climate-Related Litigation: Disclosure should include information about climate-related lawsuits, investigations, and regulatory actions.

11. Social and Environmental Justice: Companies should address climate change’s social and environmental justice implications, including impacts on vulnerable communities.

12. Insurance and Risk Management: Companies must disclose how they manage climate-related risks through insurance coverage and risk mitigation strategies.

13. Board Expertise: The rule encourages companies to disclose the expertise of their board members in climate-related matters.

14. Third-Party Verification: Companies may consider third-party verification of their climate disclosures to enhance credibility.

15. Materiality Assessment: Companies should assess the materiality of climate-related risks and opportunities based on their specific circumstances.

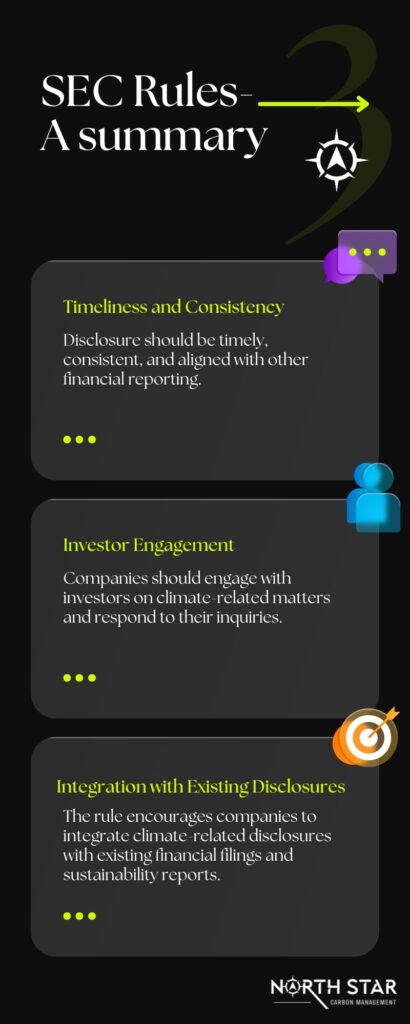

16. Timeliness and Consistency: Disclosure should be timely, consistent, and aligned with other financial reporting.

17. Investor Engagement: Companies should engage with investors on climate-related matters and respond to their inquiries.

18. Integration with Existing Disclosures: The rule encourages companies to integrate climate-related disclosures with existing financial filings and sustainability reports.

The SEC’s final disclosure rules on climate-related risks will profoundly impact industries, particularly those with significant environmental footprints, such as energy, manufacturing, and transportation. Companies in these sectors may face increased scrutiny regarding their emissions, environmental impact, and sustainability practices. The final rule also has implications for industries like finance and insurance, where climate risks significantly affect investment decisions and risk assessments by financial institutions.

To navigate these changes, industries should focus on

Engaging with stakeholders, including investors, customers, and regulatory bodies, will be crucial in aligning their business models and practices with the new disclosure requirements.

Reach out to North Star Carbon Management today to learn how our team can support your company and corporate structure to get ready for these upcoming changes. Let us make your data – simpler, sorted, and accessible with our user-friendly and modern reporting systems.

By proactively addressing these requirements, companies can comply with the new rules and position themselves as sustainability and corporate responsibility leaders.

03/11/2026

California has officially moved the market. With the adoption of SB 253 and SB 261 and the establishment of the first reporting deadline in August 2026, thousands of companies doing business in California will be required to disclose greenhouse gas emissions and climate-related financial risks. For many organizations, this will be the first time their […]

03/06/2026

The release of the GHG Protocol Land Sector and Removals Standard marks one of the most significant developments in corporate carbon accounting in over a decade. For companies involved in agriculture, forestry, fiber, food production, bioenergy, land development, apparel, consumer goods, mining rehabilitation, or carbon removal technologies, this Standard fundamentally reshapes how land-based emissions and […]

02/26/2026

For many organizations, carbon accounting does not fail because of methodology. It fails because of process. The GHG Protocol provides clear guidance on how to calculate Scope 1, Scope 2, and Scope 3 emissions. The real challenge is gathering accurate, complete, and consistent data across a complex organization without overwhelming internal teams. If your sustainability […]